In recent years, as the United States has suffered a series of damaging climate disasters, experts have warned that the nation is headed toward a homeowner’s insurance crisis. Insurance companies dropped hundreds of thousands of customers who live in areas vulnerable to hurricanes and wildfires, and numerous small insurers have gone belly-up after big disasters. This has led some to forecast that a broader market failure in disaster-prone states is looming, or even a housing market collapse.

That has not happened yet. But in the meantime, insurance has gotten a lot more expensive — and the price hikes are not going anywhere. A new nationwide report from the insurance price comparison firm Insurify found that the average American homeowner’s insurance bill rose 12 percent last year, reaching $2,948 per year, and will rise another 4 percent this year. This is much faster than overall inflation for the same period. (These numbers don’t include flood insurance, which most often requires a separate plan, backed by the federal government.)

There are a lot of factors behind these rising bills: Insurance companies consider the value of a home, the cost of the materials needed to rebuild it, and even the credit scores of the homeowner. But the primary culprits are the rising toll of extreme weather as the planet warms and the millions of new homes developers have built in vulnerable areas. Insured losses from natural catastrophes in the U.S. averaged $100 billion a year between 2023 and 2025, up from an annual average of around $15 billion per year a decade earlier, according to the Insurance Information Institute.

Change in average annual premium

“When you have these big catastrophes, it’s not just that insurers have to pay out a lot of plans, it’s that they’re all happening fast,” said Matt Brannon, the senior economic analyst at Insurify and the author of the new report. “It creates extreme financial risk for insurers, and they tend to respond to this risk by raising their rates.”

While prices are increasing in almost every state, Brannon says the most eye-watering prices are concentrated in a few regions. Below, we break down some of these hotspots using this new data. We look at where climate change and extreme weather have caused rates to surge in recent years, and which places could feel the pain next.

California

Past: 16% rise since 2023

Projected: 16% rise by the end of 2026

California is throwing everything it has at its insurance crisis, but the state government still can’t seem to move the needle. Insurance prices have gone up by 16 percent in the last two years, and are about to increase by another 16 percent this year, according to Insurify.

The state’s insurance market has been in free fall since devastating wildfire outbreaks in 2017 and 2018, which led major companies like State Farm to drop tens of thousands of mountainside customers and even pull out of the state. Regulators have coaxed insurers back by allowing them to use forward-looking “catastrophe models” that use future climate data, and by letting them pass on more of their costs to customers. In return, insurers had to stop dropping customers in fire-prone hillsides.

The only answer is to harden homes against wildfire by installing ember-proof roofs and windows and clearing vegetation to create “defensible space” around homes. Ahead of a pivotal race for insurance commissioner this year, legislators have introduced bills that would create new fire resilience grant programs and would increase coverage discounts for homeowners who retrofit their properties. It remains to be seen whether anything can stop prices from soaring higher.

Georgia

Past: 24% rise since 2023

Projected: 10% rise by the end of 2026

Hurricane Helene was among the deadliest and most expensive hurricanes ever to hit Georgia, killing 37 people, damaging tens of thousands of homes and buildings, and dealing a $5.5 million blow to the state’s agriculture and forestry industries. Those losses are driving a second year of home insurance rate hikes for Georgia, where Insurify projects a 10 percent increase in premiums in 2026 following a 9 percent increase in 2025. The impact is spread out over multiple years because of local regulations that make it tougher to quickly raise rates, according to Brannon. Neighboring Florida, by contrast, saw an 18 percent jump in 2025 because insurers were able to react quickly to heavy losses from Helene, but it is expecting more modest increases this year.

This is an ongoing pattern in Georgia, where insurers consistently collect less money in premiums than they dole out in claims, a figure known as the combined ratio. Georgia ranked third in the U.S. by that metric in 2024 and underperformed compared to the country as a whole for most of the decade before. That means that while Georgia’s rates are cheaper than many other states, they’re artificially low compared to the actual risks.

Georgia’s lagging insurance rates are now bumping up against a steep increase in damage and risk from hurricanes. Although the state’s coastline, as the Insurify report notes, is relatively small — only about 100 miles — Georgia has taken repeated hits from hurricanes in the last decade. Climate change is also spreading those impacts across much more of the state. Hurricanes and tropical storms typically weaken and break up over land, but warmer temperatures in the Gulf of Mexico are making storms stronger when they make landfall. That in turn means they remain powerful — and damaging — as they track across inland Georgia.

Joe Raedle / Getty Images

Illinois

Past: 48% rise since 2023

Projected: 5% rise by the end of 2026

Illinois may be free of the kind of wildfires and hurricanes that have roiled insurance markets on the coasts, but it has not been spared from crushing premiums. Between 2021 and 2024, home insurance costs increased by about 50 percent in Illinois, costing homeowners close to an additional $1,000 per year, according to a Consumer Federation of America report.

State Farm, the largest home insurer in the country, announced plans to raise homeowner insurance rates by over 27 percent across the state last summer. Not far behind, Allstate, the nation’s second-largest home insurer, filed for increases totaling 9 percent on average for over 200,000 Illinois policyholders. Both of the insurance giants pointed to extreme weather as driving up costs — in 2024, only Texas reported more hail damage than Illinois, according to State Farm.

Last month, during his budget proposal to Illinois legislators, Governor JB Pritzker railed against a steady stream of homeowner insurance rate hikes, calling the spiraling costs “nothing short of a crisis.” Currently, Illinois is the only state in the country without legislation prohibiting excessive rates. Legislators failed to pass a bill limiting price hikes last fall, but Pritzker is still urging the General Assembly to revive the bill. In the meantime, insurance premiums may continue to climb. Insurify forecasts another 5 percent surge this year.

Michigan

Past: 36% rise since 2023

Projected: 3% rise by the end of 2026

The Great Lakes state saw a nearly 36 percent increase in insurance prices in the last two years, thanks to two factors: insurance companies absorbing losses from other parts of the country and an uptick in severe weather like thunderstorms, ice storms, flooding, and hail. Michigan is seeing more of these “secondary perils” that often generate a large number of low- to mid-range claims. Every year since 2011, the state has experienced at least one severe storm where losses exceeded $1 billion, according to the National Oceanic and Atmospheric Administration. In 2024, five such storms occurred.

But despite recent hikes, Insurify notes that Michigan still has some of the lowest average premiums in the Midwest. Prices in 2026 will stabilize slightly after two years of hikes, projected to rise by 3 percent. These fluctuations, especially in the Midwest, are the result of companies figuring out how to price changing risk, according to insurance experts. “They’re trying to adjust their pricing to cover the potential costs,” said Andy Hoffman, a professor of sustainable enterprise at the University of Michigan. “They may raise their rates. They don’t have the payouts. They have to adjust them back.”

Nebraska

Past: 20% rise since 2023

Projected: 13% rise by the end of 2026

Going back over 10 years, Nebraska has seen some of the highest rates of increases in home insurance premiums in the country, said Eric Hunt, assistant extension educator of agricultural meteorology and climate resilience at the University of Nebraska Extension. Over the past year alone, premiums jumped 25 percent on average, according to data from Insurify.

Currently, Nebraska allows companies to set premiums based on market rates, rather than getting approval or being capped by state regulators. That system is one of the reasons why insurance has gotten so expensive.

The rise in rates also correlates with the state’s severe storms, which bring damage from increased hail and high winds. The city of Lincoln, for example, faced severe hail back in May 2016, and multiple damaging windstorms have hit both Lincoln and Omaha in the last five years. As the climate continues to change, Nebraska could see more of these severe storms, in addition to potentially more heavy rain events that can cause flash flooding.

There’s another risk that’s also emerging: Nebraska is getting less snow than it used to, worsening the state’s wildfire season. Paired with more days with high wind gusts, “I think, especially in the western part of the state, I think you’re going to see smaller towns be more vulnerable to those fires,” Hunt said.

As insurance rates gain more attention from state politicians, Hunt said he expects there to be more attempts to regulate increases in Nebraska.

North Carolina

Past: 14% rise since 2023

Projected: 5% rise by the end of 2026

North Carolina has had an interesting few years when it comes to insurance premiums. The state’s rate bureau asked for a 42 percent rate hike last year, citing both increased, risky development in hurricane-prone coastal areas and billions in storm damage from Hurricane Helene, but the state insurance commissioner granted just a 7.5 percent increase. Now, Insurify projects North Carolina’s insurance premiums to rise in 2026 by about 5 percent. Compared to other high climate-risk states, that’s not a lot — but there’s more to the story.

Much of the damage incurred by North Carolina homeowners over the past several years is flood damage from extreme, multi-billion-dollar storms like Helene in Western North Carolina and Florence in the coastal region, but flood damage is not covered by homeowners’ insurance.

Other storm damage is coverable in certain cases, like wind-related tree damage, but that too is proving to be problematic. “In North Carolina and in higher-risk coastal states, insurers are not providing coverage, like in your base home policy plan, for things like high wind damage,” said Jayson O’Neill, a spokesperson for Unlocking America’s Future, which recently released a report on North Carolina’s insurance trends. A quarter of homeowners’ insurance claims after Helene were closed without payment last year. Furthermore, some insurance companies are abandoning the state, or risk-prone swaths of it, entirely. Nationwide, for example, dropped 10,000 customers in hurricane-prone zip codes of coastal North Carolina in 2024. O’Neill believes these denials keep rate increases on the moderate side — with upfront costs to homeowners.

Finally, a “consent to rate” loophole in the state allows companies to directly ask homeowners to approve monthly increases, which can open the door to future increases for individual households.

It’s a delicate balance, according to Mike Causey, the state’s Commissioner of Insurance. “You can’t run the companies out of business, or we’d all be in trouble,” Causey said. “So, we’ve been trying to keep the increase as close to zero as possible.”

There is no easy way out of this problem, no matter what disasters a state is facing. State regulators can’t just refuse insurance companies permission to raise prices, because then those companies will drop customers or leave the market altogether, as has happened in California. Many states offer their own “public option,” such as Florida Citizens and the California FAIR Plan, but these backstops tend to provide worse coverage, and they’re often more expensive than the private market. Such options can also pull money from a state’s tax base, which raises a fairness issue — why should every taxpayer have to fund insurance for those who live in the most expensive and disaster-prone homes?

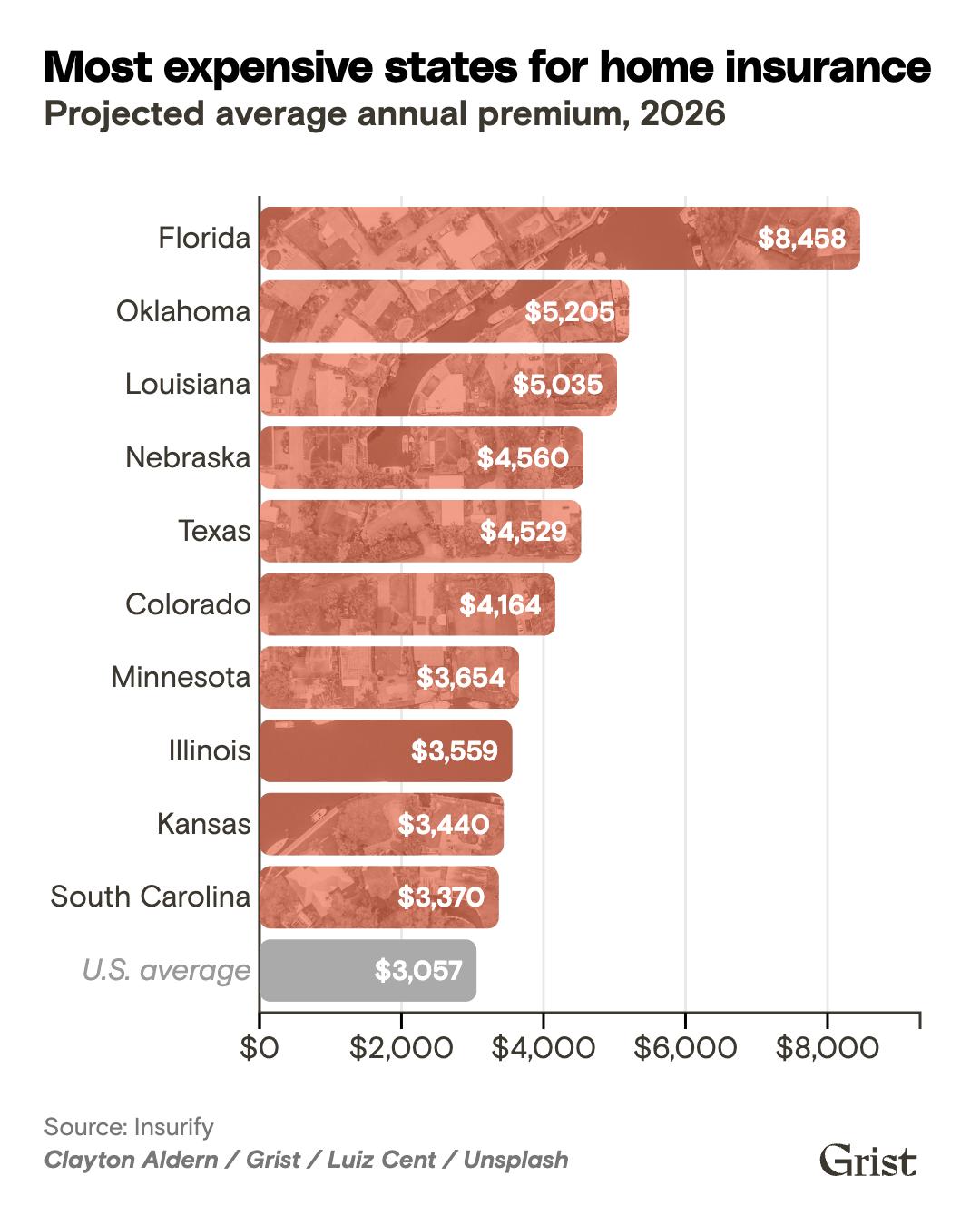

Projected average annual premium, 2026

The only real solution to rising prices — other than slowing down climate change itself — is to reduce the amount of property that is at risk from natural disasters. That entails renovating, rebuilding, or relocating millions of properties across dozens of states until major disasters no longer cause billions of dollars in damages. The cost of disasters such as flooding has gone down over the last century when compared against the value of property exposed to those disasters, indicating that some adaptation has already happened, but it needs to happen even faster.

A recent report from the Natural Resources Defense Council predicted the U.S. could be “an uninsurable country” if no action is taken, and Democratic Senator Sheldon Whitehouse warned that the insurance collapse could cause a “2008 or worse” recession.

The question is who should pay for this. Most individual homeowners don’t have thousands of dollars to spend on new roofs and walls, and states don’t have billions of dollars to hand out for retrofits. Developers tend to resist building codes that require tougher homes, and insurance companies themselves are hesitant to pay for customer upgrades and then have their customers depart for other providers, depriving the insurer of any cost savings.

Brandon Bell / Getty Images

The solution may be some mix of all these policies. In another recent report from the Natural Resources Defense Council, researchers argue that states should impose surcharges on their insurers and use the money to fund roof upgrades and vegetation clearance, targeting the most vulnerable homes that are driving claims. North Carolina and Alabama have both scaled such programs. Lawmakers could also upgrade building rules for new homes, imposing a cost on developers, as Florida did following Hurricane Andrew in 1992. Meanwhile, the legislature in Colorado has weighed creating a state-run “reinsurance” program, which would provide a financial backstop for smaller insurers and reduce their costs.

But until we reduce the risk profile of the nation’s homes, the price increases are unlikely to stop, according to Carolyn Kousky, an expert on disaster insurance and former University of Pennsylvania economist who runs the Insurance For Good project, which advocates for just disaster insurance frameworks.

“We see in the hotspots of climate risk that the premiums have even outpaced [other costs],” she said. “Until we actually focus much more heavily on loss reduction and climate adaptation, that will continue to be a challenge.”

:max_bytes(150000):strip_icc()/Health-GettyImages-Repub-Amaranth-6865d7e102c0494491505f91825e5ec5.jpg?w=390&resize=390,220&ssl=1 "What Happens to Your Body When You Eat Amaranth Regularly")